Letters of CreditLetters of Credit

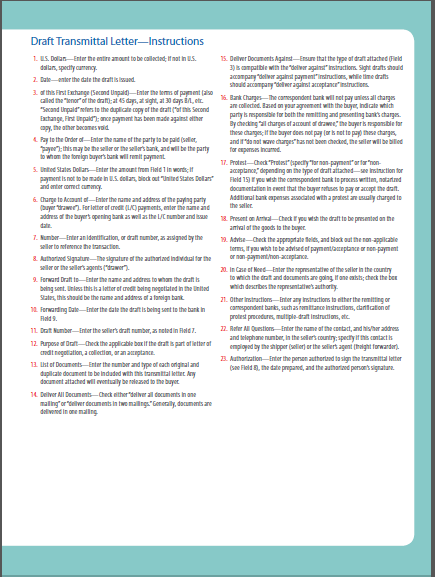

Letters of credit or documentary collections, which are also commonly known as drafts, are often used to protect the interests of both buyer and seller. These two methods require that payment be made on presentation of documents conveying the title and showing that specific steps have been taken. Letters of credit and drafts may be paid immediately or at a later date. Drafts that are paid on presentation are called sight drafts. Drafts that are to be paid at a later date, often after the buyer has received the goods, are called time drafts or date drafts. The parties rely on a transmittal letter, which contains complete and precise instructions on how the documents should be handled and how the payment is to be made (see Appendix D for sample form).

Because payment by these two methods is made on the basis of documents, you should avoid confusion and delay by specifying all terms of payment clearly. For example, “net 30 days” should be specified as “30 days from acceptance.” Likewise, the currency of payment should be specified as “US $30,000.” International bankers can offer other suggestions.

Banks charge fees—mainly based on a percentage of the amount of payment—for handling letters of credit and smaller amounts for handling drafts. If fees charged by both the foreign and U.S. banks are to be applied to the buyer’s account, this term should be explicitly stated in all quotations and in the letter of credit.

The exporter usually expects the buyer to pay the charges for the letter of credit. If, however, the buyer does not agree to this added cost, you must either absorb the costs of the letter of credit or risk losing that potential sale. Letters of credit for smaller amounts can be somewhat expensive because fees can be high relative to the sale.

A letter of credit may be irrevocable, which means that it cannot be changed unless both parties agree. Alternatively, it can be revocable, in which case either party may unilaterally make changes. A revocable letter of credit is inadvisable because it carries many risks for the exporter. To expedite the receipt of funds, you can use wire transfers. You should consult with your international banker about bank charges for such services.

When preparing quotations for prospective customers, you should keep in mind that banks pay only the amount specified in the letter of credit—even if higher charges for shipping, insurance, or other factors are incurred and documented.

On receiving a letter of credit, you should carefully compare the letter’s terms with the terms of the pro forma quotation. This step is extremely important because if the terms are not precisely met, the letter of credit may be invalid and you may not be paid. If meeting the terms of the letter of credit is impossible, or if any of the information is incorrect or even misspelled, you should contact the customer immediately and ask for an amendment to the document. You must provide documentation showing that the goods were shipped by the date specified in the letter of credit; otherwise, you may not be paid. You should check with your freight forwarders to make sure that no unusual conditions that would delay shipment can reasonably be anticipated.Documents must be presented by the date specified. To ensure that the letter of credit will be paid, you should verify with your international banker that there will be sufficient time to present the documents required for payment.You may request that the letter of credit specify that partial shipments and transshipment will be allowed. Specifying acceptable practices can prevent unforeseen problems at the last minute.

nonpayment. Documentary collections are generally less expensive than letters of credit.

In practice, the ocean bill of lading is endorsed by the exporter and sent by the exporter’s bank to the buyer’s bank. It is accompanied by the sight draft, invoices, and other supporting documents that are specified by either the buyer or the government of the buyer’s country (e.g., packing lists, commercial invoices, and insurance certificates). The foreign bank notifies the buyer when it has received these documents. As soon as the draft has been paid, the foreign bank turns over the bill of lading, thereby enabling the buyer to obtain the shipment.

There is still some risk when a sight draft is used to control the transfer of title of a shipment. For example, the buyer’s ability or willingness to pay might change between the time the goods are shipped and the time the drafts are presented for payment. Moreover, the buyer’s obligation is not backed up by a bank promise to pay. There is also the possibility that the policies of the importing country will change. In the end, if the buyer cannot or will not pay for and claim the goods,returning or disposing of the products becomes the problem of the exporter.

A date draft differs slightly from a time draft in that it specifies a date on which payment is due, rather than a time period after acceptance of the draft. When either a sight draft or a time draft is used, a buyer can delay payment by delaying acceptance of the draft. A date draft can prevent this delay in payment, though the document still must be accepted.

Because payment by these two methods is made on the basis of documents, you should avoid confusion and delay by specifying all terms of payment clearly. For example, “net 30 days” should be specified as “30 days from acceptance.” Likewise, the currency of payment should be specified as “US $30,000.” International bankers can offer other suggestions.

Banks charge fees—mainly based on a percentage of the amount of payment—for handling letters of credit and smaller amounts for handling drafts. If fees charged by both the foreign and U.S. banks are to be applied to the buyer’s account, this term should be explicitly stated in all quotations and in the letter of credit.

The exporter usually expects the buyer to pay the charges for the letter of credit. If, however, the buyer does not agree to this added cost, you must either absorb the costs of the letter of credit or risk losing that potential sale. Letters of credit for smaller amounts can be somewhat expensive because fees can be high relative to the sale.

Letters of Credit

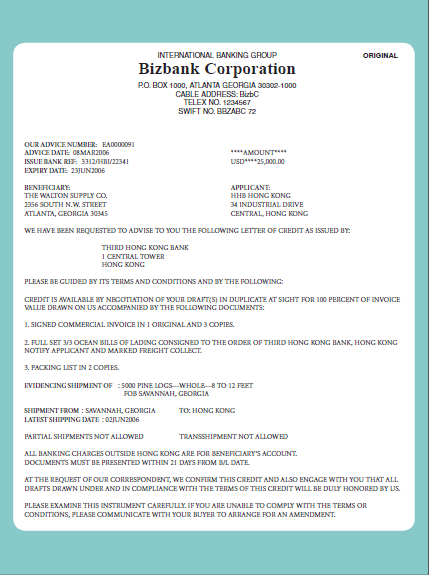

Letters of credit are one of the most versatile and secure instruments available to international traders. A letter of credit is a commitment by a bank on behalf of the importer (foreign buyer) that payment will be made to the beneficiary (exporter), provided the terms and conditions stated in the letter of credit have been met, as evidenced by the presentation of specified documents. A letter of credit issued by a foreign bank is sometimes confirmed by a U.S. bank. This confirmation means that the U.S. bank (the confirming bank) has added its promise to that of the foreign bank (the issuing bank) to pay the exporter. If a letter of credit is not confirmed, it is “advised” through a U.S. bank, and thus the document is called an advised letter of credit. U.S. exporters may wish to have letters of credit issued by foreign banks confirmed through a U.S. bank if they are unfamiliar with the foreign bank or are concerned about the political or economic risk associated with the country in which the bank is located. A U.S. Commercial Service office or international banker can assist exporters in evaluating the risks to determine what terms might be appropriate for a specific export transaction.A letter of credit may be irrevocable, which means that it cannot be changed unless both parties agree. Alternatively, it can be revocable, in which case either party may unilaterally make changes. A revocable letter of credit is inadvisable because it carries many risks for the exporter. To expedite the receipt of funds, you can use wire transfers. You should consult with your international banker about bank charges for such services.

| Letters of credit, also referred to as drafts, are used to help protect both the buyer and the seller. |

A Typical Letter of Credit Transaction

Here are the typical steps in issuing an irrevocable letter of credit that has been confirmed by a U.S. bank:- After the exporter and the buyer have agreed on the terms of a sale, the buyer arranges for its bank to open a letter of credit that specifies the documents needed for payment. The buyer determines which documents will be required.

- The buyer’s bank issues (opens) its irrevocable letter of credit and includes all instructions to the seller relating to the shipment.

- The buyer’s bank sends its irrevocable letter of credit to a U.S. bank and requests confirmation. The exporter may request that a particular U.S. bank be the confirming bank, or the foreign bank may select a U.S. correspondent bank.

- The U.S. bank prepares a letter of confirmation to forward to the exporter, along with the irrevocable letter of credit.

- The exporter carefully reviews all conditions in the letter of credit. The exporter’s freight forwarder is contacted to make sure that the shipping date can be met. If the exporter cannot comply with one or more of the conditions, the customer is alerted at once because an amendment may be necessary.

- The exporter arranges with the freight forwarder to deliver the goods to the appropriate port or airport.

- When the goods are loaded aboard the exporting carrier, the freight forwarder completes the necessary documentation.

- The exporter (or the freight forwarder) presents the documents, evidencing full compliance with the letter of credit terms, to the U.S. bank.

- The bank reviews the documents. If they are in order, the documents are sent to the buyer’s bank for review and then transmitted to the buyer.

- The buyer (or the buyer’s agent) uses the documents to claim the goods.

- A sight or time draft accompanies the letter of credit. A sight draft is paid on presentation; a time draft is paid within a specified time period.

Tips on Using Letters of Credit

When preparing quotations for prospective customers, you should keep in mind that banks pay only the amount specified in the letter of credit—even if higher charges for shipping, insurance, or other factors are incurred and documented.

On receiving a letter of credit, you should carefully compare the letter’s terms with the terms of the pro forma quotation. This step is extremely important because if the terms are not precisely met, the letter of credit may be invalid and you may not be paid. If meeting the terms of the letter of credit is impossible, or if any of the information is incorrect or even misspelled, you should contact the customer immediately and ask for an amendment to the document. You must provide documentation showing that the goods were shipped by the date specified in the letter of credit; otherwise, you may not be paid. You should check with your freight forwarders to make sure that no unusual conditions that would delay shipment can reasonably be anticipated.Documents must be presented by the date specified. To ensure that the letter of credit will be paid, you should verify with your international banker that there will be sufficient time to present the documents required for payment.You may request that the letter of credit specify that partial shipments and transshipment will be allowed. Specifying acceptable practices can prevent unforeseen problems at the last minute.

Documentary Collections

A documentary collection is a transaction whereby the exporter entrusts the collection of the payment for a sale to its bank (remitting bank), which sends the documents its buyer needs to the importer’s bank (collecting bank), with instructions to release the documents to the buyer for payment. In exchange for these documents, funds are received from the importer and remitted to the exporter through the banks involved in the collection. Documentary collections involve using a draft that requires the importer to pay the face amount either at sight (document against payment) or on a specified date (document against acceptance). The collection letter specifies the documents required for the transfer of title to the goods. Although banks do act as facilitators for their clients, documentary collections offer no verification process, and there is limited recourse in the event ofnonpayment. Documentary collections are generally less expensive than letters of credit.

Documents against Payment Collection

A document against payment collection, also known as a sight draft, is used when the exporter wishes to retain title to the shipment until it reaches its destination and payment has been made. Before the shipment can be released to the buyer, the original “order” for the ocean bill of lading (the document that evidences title) must be properly endorsed by the buyer and surrendered to the carrier. It is important to note that the buyer can claim the goods without presenting air way bills. Risk increases when a sight draft is used with an air shipment.In practice, the ocean bill of lading is endorsed by the exporter and sent by the exporter’s bank to the buyer’s bank. It is accompanied by the sight draft, invoices, and other supporting documents that are specified by either the buyer or the government of the buyer’s country (e.g., packing lists, commercial invoices, and insurance certificates). The foreign bank notifies the buyer when it has received these documents. As soon as the draft has been paid, the foreign bank turns over the bill of lading, thereby enabling the buyer to obtain the shipment.

There is still some risk when a sight draft is used to control the transfer of title of a shipment. For example, the buyer’s ability or willingness to pay might change between the time the goods are shipped and the time the drafts are presented for payment. Moreover, the buyer’s obligation is not backed up by a bank promise to pay. There is also the possibility that the policies of the importing country will change. In the end, if the buyer cannot or will not pay for and claim the goods,returning or disposing of the products becomes the problem of the exporter.

| Familiarize yourself with the different tools and options for transmission of payment. Some will save you time and money,others will increase security. |

Document against Acceptance Collection

A document against acceptance collection, also known as a time draft, is used when the exporter extends credit to the buyer. The draft states that payment is due by a specific time after the buyer has accepted the time draft and received the goods. By signing and writing “accepted” on the draft, the buyer is formally obligated to pay within the stated time. When this is done, the time draft is then called a trade acceptance. It can be kept by the exporter until maturity or sold to a bank at a discount for immediate payment.A date draft differs slightly from a time draft in that it specifies a date on which payment is due, rather than a time period after acceptance of the draft. When either a sight draft or a time draft is used, a buyer can delay payment by delaying acceptance of the draft. A date draft can prevent this delay in payment, though the document still must be accepted.